Following the publication of the paper (noted below) on the epithermal portion of the Recsk metallogenic system in Hungary here are 3D models from the entirely concealed Cu-Au mineralized intrusive bodies and related Cu-Au skarns and outbound Zn-Pb replacement bodies.

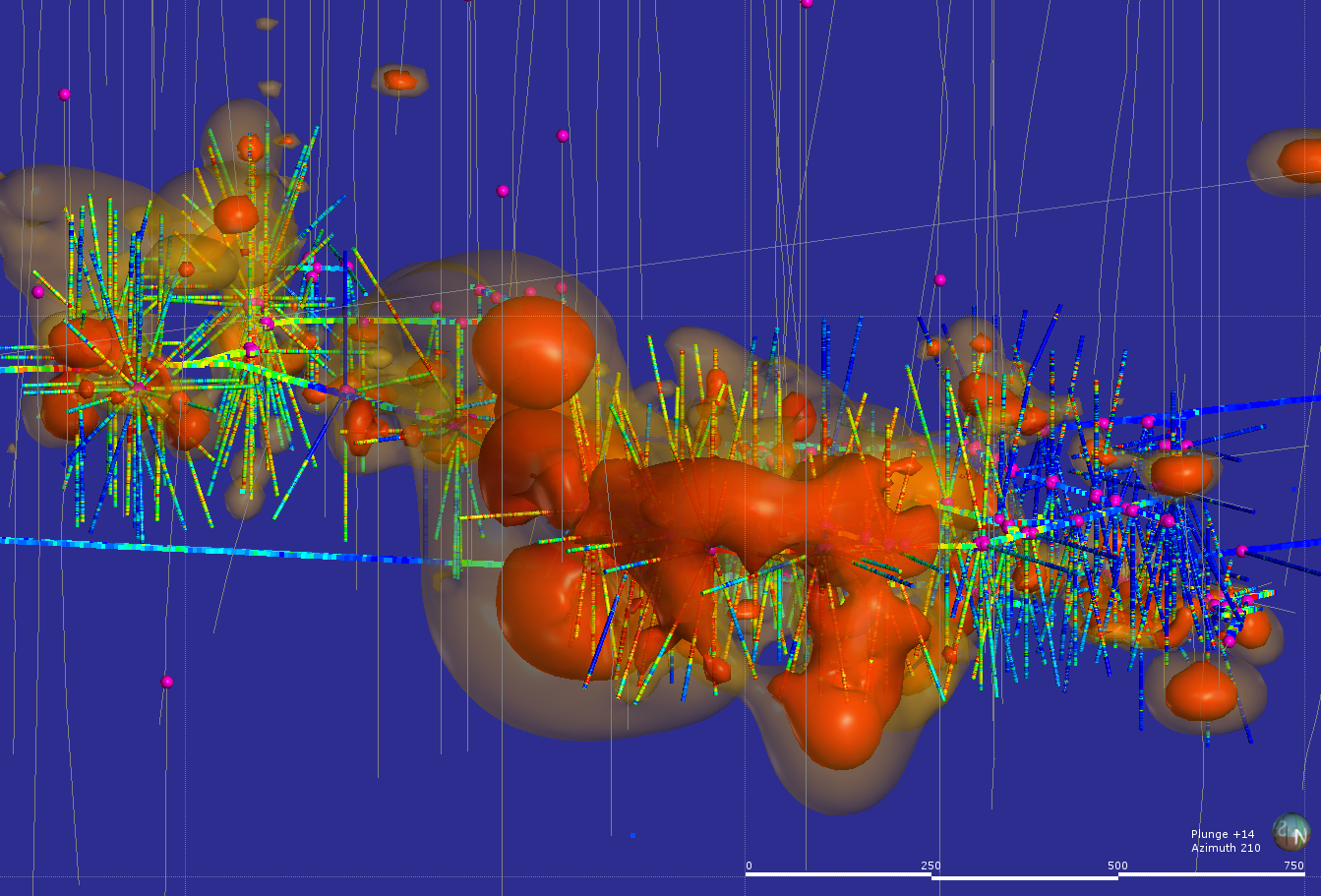

A 3D fly-though of the Recsk Cu-Au deposit showing the drilling, channel samples and interpolated copper grade shells. A full set of 100 metre spaced section steps through the deposit from north to south over several kilometres.

A section through the Recsk deposit with drilling and copper grade shells. The section is 200 metres thick and the 0.3% grade shell is 800 metres high and 1,000 metres wide. The Cu-Au skarn mineralisation can be seen dipping gently away from the large intrusive body. The intrusion is open at depth below 1,200 metres. The top of the 10.3% copper grade shell is approximately 400 metres below the surface.

This 3D Model is based upon 156,000 metres of surface drilling over 35 square kilometres, 9km of underground development and 90,000 metres of underground drilling.

The Recsk metallogenic centre consists of a deep and entirely preserved mineralised intrusive and intermediate and high sulphidation epithermal deposits exposed at surface. The epithermal deposits are located close to the apex of the intrusion. The diorite intrusion is hosted by a thick sequence of Eocene carbonates unconformably overlain by a volcanic edifice. Adjacent to the intrusion the carbonates host thick Cu-Au skarns. Outbound of the Cu-Au skarns, Zn-Pb replacement bodies have been intersected in wide spaced drillholes. In this video we present a section through the deposit. The 3D model is based upon 156,000 metres of drilling from surface, 9 km of underground sampling on the 700 and 900 metre levels and 89,000 metres of underground diamond drilling. Underground access was provided by two 1,200 metre deep shafts, 2,000 metres apart. The shafts have an 8 metre internal diameter and are concrete lined. No mining has been undertaken at the deeper Recsk mineralisation aside from bulk metallurgical sampling.

Ivanhoe Mines has released its much anticipated DFS on its US$1.544 billion Platreef 4 Elements (4E-platinum, palladium gold and rhodium) project in South Africa (DFS yet to be released on Sedar).

Ivanhoe #2 shaft sink in progress

Key features of the Platreef DFS include:

Indicated Mineral Resources at a 2 g/t 4E COG are 346 million tonnes at 1.7 g/t Pt, 1.7 g/t Pd, 0.1 g/t Rh and 0.3 g/t Au for 42 million ounces of Pt, Pd, Rh and Au with an additional 53 million ounces in Inferred Resources;

Mineral Reserve containing 17.6 million ounces of platinum, palladium, rhodium and gold;

Development of a large, mechanized, underground mine with an initial 4 Mtpa concentrator and associated infrastructure with plans to increase production incrementally to 12 MTPA;

Planned initial average annual production rate of 476,000 ounces of Pt, Pd, Rhand Au(3PE+Au), plus 9,500 tonnes of nickel and 5,900 tonnes of copper in concentrates;

174 kt of concentrate will be produced at 38 g/t Pt, 39.1 g/t Pd, 2.4 g/t Rh, 5.3 g/t Au, 3.35 Ni and 5.5% Ni;

Estimated pre-production capital requirement of approximately US$1.544 billion, at a ZAR:USD exchange rate of 13 to 1.

After-tax Net Present Value (NPV) of US$916 million, at an 8% discount rate.

After-tax Internal Rate of Return (IRR) of 14.2%.

The 14% IRR is less than appealing and they only got there by using some snappy metal prices: US$1,250 per ounce (current price $945) for Pt, $815/Oz ($835) for Pd, $1,300/ozs ($1,270) for Au and $1,000/oz ($900-990) for Rh.

Net total cash cost + SIB capital (2017 mines in production and selected projects), US$/3PE+Au oz.

So how to finance this project. Ivanhoe owns 64%, their Black Economic Empowerment (BEE) partner 26% and a Japanese consortium 10%. New legislation would see the BEE percentage increase to 30% and that has to be financed. Given the evolving political uncertainty in SA there might be some investor hesitation for a project in that country and which has a 14% IRR. We will watch with the usual interest.

Exciting news for Barrick and Antofagasta, after years of frustration. B&A reportedly spent US$500 million on this project and were refused a mining lease and licence to operate by the Government of Baluchistan. Compensation for loss is going to be a most interesting hearing. This is a remarkably robust project and a very long lived mine. This is why we offered B&A US$200 million a few years ago in an attempt to resolve the matter – Good for them they they stuck out the challenge of arbitration.

TORONTO, March 21, 2017 — Barrick Gold Corporation (NYSE:ABX)(TSX:ABX) (“Barrick” or the “Company”) announced that an arbitration tribunal of the World Bank’s International Center for Settlement of Investment Disputes (“ICSID”) yesterday issued a decision on the arbitration claims that Tethyan Copper Company Pty Limited (“TCC”), a joint venture between Antofagasta plc and Barrick, filed against the Islamic Republic of Pakistan, in relation to the unlawful denial of a mining lease for the Reko Diq project in 2011.

Yesterday’s decision by the ICSID tribunal rejected Pakistan’s final defense against liability, and confirmed that Pakistan had violated several provisions of its bilateral investment treaty with Australia, where TCC is incorporated.

The damages phase of the proceedings will begin on March 22, during which the tribunal will consider submissions from the parties to determine the amount that Pakistan must pay TCC. A ruling on the quantum of damages is expected in 2018.

The Reko Diq project, located in the Balochistan province of Pakistan, was expected to require an initial capital investment of more than $3 billion. It is one of the world’s largest undeveloped copper and gold deposits, with a potential mine life of more than 50 years.

Commentary

Mineralisation in the Reko Diq area

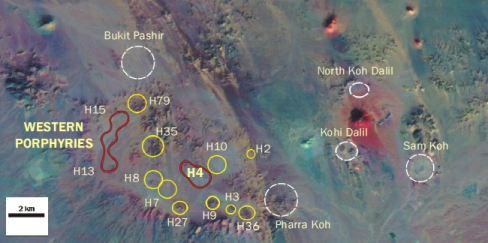

Reko Diq is a large (10×10 km) volcano-magmatic complex located in the western Chagai magmatic belt in Pakistan. Over 48 porphyry Cu-Au centres are recognized in the Chagai belt. Twenty of them, including the world-class H14-H15 cluster, are located in the Reko Diq district. These deposits are largely associated with four consecutive episodes of magmatism during the Miocene. The porphyry centres are characterized by stocks and dyke swarms of diorite, quartz diorite and granodiorite composition. The deposits offer no technological development challenges. Reko Diq is located 50 kilometres to the east of the 300 million tonne Saindak porphyry copper gold deposit being operated by Metallurgical Corporation of China since 2002 under a lease agreement with the Government of Pakistan.

Deposit Geology

The Reko Diq porphyry district hosts a cluster of 20 Cu-Au porphyry centres in an area approximately 10×10 km bounded by the NW trending fault systems of Drana Koh in the north and Tuzgi Koh in the south.

The underlying volcano-sedimentary rocks at Reko Diq consist of thin-bedded shale, siltstone, shallow marine to fluviatile sandstone and minor discontinuous conglomerate and lava flow of the late Oligocene Dalbandin and Eocene Saindak Formations. The porphyry Cu-Au centres at Reko Diq are spatially and genetically associated with early to late Miocene calc-alkaline diorite, quartz diorite and granodiorite intrusions.

Hydrothermal alteration at Reko Diq is typical of porphyry Cu deposits. The porphyry centres at H14-H15 are characterized by a central potassic zone surrounded by phyllic (quartz-sericite-pyrite) and outer propylitic (chlorite-epidote) alteration. The main ore stage (chalcopyrite±bornite) mineralization is generally disseminated in host the porphyries and occurs in veinlets with a total sulphide content of 2-3 vol. percent. The chalcopyrite to pyrite ratio decreases at shallow levels. A distinct late stage pyrite+chacopyrite±molybdenite assemblage associated with D-veins is common in most of the porphyry systems at Reko Diq. The bornite to chalcopyrite ratio increases with the intensity of potassic alteration and magnetite content, which gives rise to higher Cu-Au grades (0.8% Cu; 0.6 g/t Au) in the deep central part of the deposits. A high sulfidation type assemblage of covellite+bornite+pyrite in association with quartz+sericite±kaolinite alteration is identified mainly in the sandstone and conglomerate units of the H15 system. Overall, a metal zoning from Cu-Au at the center and depth with potassic alteration and increasing Mo in the margins and upper parts of the porphyry system at H14-H15, can be defined.

The supergene oxidation is commonly very weak in the district with leached zone of less than a few meters. The only supergene enriched Cu blanket at Reko Diq is preserved in the central Tanjeel porphyry Cu deposit in which an irregular, 50 to 100m-thick chalcocite blanket, is developed beneath a 40-50m-thick leached cap dominated by jarosite and local hematite. The chalcocite blanket (0.5-1.0% Cu) has a gradational lower contact with low grade hypogene Cu-Fe-sulfide mineralization at depth.

Exploration History

Regional exploration for porphyry copper mineralization was initiated in 1993, when BHP Minerals signed a joint venture mineral exploration agreement with the Baluchistan Development Authority, over an area of 13,000 km2. Following an orientation survey over the Saindak deposit, regional geochemical exploration using −80 mesh and the bulk leachable gold (BLEG) method was conducted from 1993 to 1995, with the collection of approximately 5,000 samples. Sixteen anomalous areas were defined and follow-up work, including geologic mapping and standard rock geochemistry, was carried out over them. This work delineated 14 prospective areas, of which Reko Diq, Ziarat Pir Sultan, Ting-Dargun, Kirtaka, Machi, Dasht-e-Kain, Koh-i-Sultan, Durban Chah, and Ganshero were judged to be the most promising. Additional mapping, rock geochemistry, and ground magnetics were completed from 1996 to 1998, followed by 20,000 m of reverse circulation and core drilling. This program resulted in the discovery of the Reko Diq porphyry copper cluster, including the supergene enrichment blanket at Tanjeel (originally named H4) and the nearby hypogene copper-gold deposits at H14-H15 (also referred to as Western Porphyries), H8, and H13.

Geophysical surveys, both induced polarization and magnetics, were completed over them. These and other targets were drilled in several short programs during 2003 to 2006, for a total of approximately 48,000 m, including 24,000 m of infill drilling at Tanjeel. The new resource for Tanjeel, announced in late 2006, was 126 million metric tons (Mt) at 0.7 percent Cu, all leachable supergene-enriched sulfides. In 2006, a joint venture between Antofagasta Minerals S.A. and Barrick Gold Corp. acquired 100 percent of Tethyan Copper Company and its 75 percent interest in the Reko Diq and regional licenses and initiated an aggressive infill drilling program and scoping study at H14-H15. Resource drilling during 2006 to 2009 at Reko Diq totaled approximately 136,000 m resulting in completion of a feasibility study during 2010 for a 110,000 tonne per day operation producing copper-gold concentrate for export.

Reserves and Resources

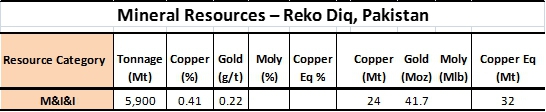

Reko Diq is one of the largest known undeveloped copper-gold porphyries with resources of 5.9 billion tonnes at 0.41% copper and 0.22 g/t gold for 54 billion pounds of copper and 42 million ounces of gold. Within this resource is a high grade zone with 400 million tonnes at 0.9% copper and 0.6 g/t gold and a supergene resource at Tanjeel of 214 million tonnes at 0.6% copper. Significant potential exists within the Reko Diq porphyry cluster for expansion of this resource and a number of targets remain only lightly explored.

Reko diq resources – a very significant deposit

Planned Development

The planned development included a conventional open pit mining operation utilizing hydraulic face shovels and trucks feeding a conventional concentrator utilizing industry standard crushing, grinding and flotation. Tailings will be deposited in a engineered TMF.

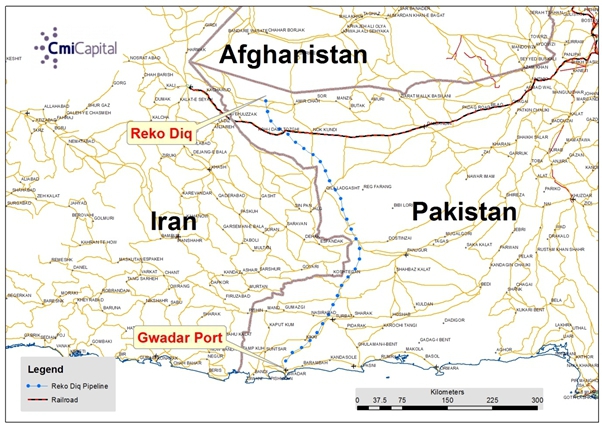

Location of the Reko diq deposit and infrastructure – or lack therof

Power will be provided by a purpose-built 190 MW power station adjacent to the mill faculty.

The Reko Diq deposit produces a clean high grade concentrate with 28-31% copper and 7-22 g/t gold. Concentrate at a 52% pulp density will be pumped via a 682 km buried slurry pipeline to the port of Gwadar presently being redeveloped by a Chinese company.

At Gwadar Port a de-watering facility using high pressure filters will produce a concentrate with 7.5% water, which will be conveyed to a portside warehouse. A conveyor and ship loader will also be constructed.

Project Cashflow Analysis

Cmi Capital constructed a cashflow model based upon available information with costs from comparable recent projects. Two models were evaluated, a base case model with an open pit mine and conventional mill treating 120,000 tonnes per day (TPD) and an expanded model with a production rate of 200,000 TPD after year 5. These models with mine lives of 30 years consume only 21% to 33% respectively of the existing resource. In addition there is potential for the exploitation of higher grades in the early years, the discovery of additional reserves and the addition of a dump leach SXEW facility to treat the large Tanjeel supergene copper deposit (240 Mt at 0.6% leachable copper).

This analysis (with the cashflow models limited to 30 years) indicates that Reko Diq is an economically robust, long life project as can be seen below (metal prices used were a few years ago).

Copper Production: 162,000 to 257,000 TPY

Gold Production: 260KOz to 408kOz PA

NPV (08): US$2 to 3.4 billion (at long term metal pricing)

IRR: 15% to 17%

An outstanding project that has potential to significantly improve the outcomes for the peoples of Baluchistan and bring much needed development to a very challenging part of the country.

Mining Journal is remarkably bullishon the Ilovitza project in Macedonia. John C. Menzies, CEO of Cmi Capital Limited was previously the CEO of Euromax and built the company and its exploration assets over an 8 year period.

The Ilovtiza mine is planned for the back of the large bald mountain behind the villages of Ilovitza and Stuka in Macedonia

The Ilovitza mine is planned for the back of the large bald mountain behind the villages of Ilovitza and Stuka in Macedonia\n\n\”Multi-billion-dollar returns from a world class gold-copper resource are usually the preserve of mining’s majors, not a minnow. But they are exactly what investors in Euromax Resources (TSX: EOX) have to look forward to from the US$475 million Ilovica project in Macedonia, which is ready to move forward in what president and CEO Steve Sharpe describes as an ideal environment for building major new mining projects.\n\n“This is exactly the time to be building a copper-gold mine of this size because the amount of chits that are being offered to us now in terms of major capital items that would normally be the long lead stuff,” he says. “The offers are coming from mining companies, from suppliers that have cancelled orders, and this is all brand new equipment at a fraction of the retail price or list price. So I expect to see some fairly chunky capex and operational savings.”

Production is slated at 83,000 oz pa of gold and 16,000tpa of copper, starting in 2018, with overall average process recoveries at 83.3% for gold and 81.3% for copper”.

Ilovitza is a Tertiary porphyry copper-gold deposit and is ideally situated for development being close to services, water and infrastructure. The measured and indicated resources total 250 million tonnes containing 2.6 M ounces of gold and 550,000 tonnes of copper. While the grade is low, the low stripping ratio, low infrastructure capital and operating costs and proximity to rail and smelters reports an attractive NPV and IRR in the feasibility study.